At the Federal Energy Regulatory Commission’s (“FERC” or the “Commission”) monthly open meeting on February 19, 2026, the Commission reaffirmed that it will not reinstate its ban on gas pipeline work during appeals.

At the Federal Energy Regulatory Commission’s (“FERC” or the “Commission”) monthly open meeting on February 19, 2026, the Commission reaffirmed that it will not reinstate its ban on gas pipeline work during appeals.

The Internal Revenue Service (the “IRS” or “Service”) recently released detailed guidance concerning the classification and treatment of Prohibited Foreign Entities (“PFEs”) as well as the application of the related Foreign Entity of Concern (“FEOC”) restrictions that were created in the One Big Beautiful Bill Act (“OBBBA” or “Bill”).

Enacted by the Inflation Reduction Act and recently amended by the One Big Beautiful Bill Act (“OBBBA”), Section 45Z of the Internal Revenue Code offers a tax credit for the domestic production and sale of certain low-emission transportation fuels (“45Z Credit”). The 45Z Credit is worth $0.20 (or $1.00 for producers meeting prevailing wage and apprenticeship requirements) per gallon of renewable diesel, sustainable aviation fuel (“SAF”), renewable natural gas (“RNG”), and certain other low-carbon fuels produced domestically and sold.

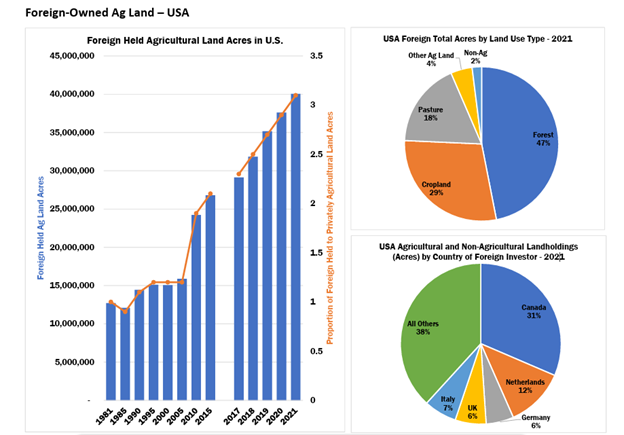

In recent years, the U.S. government has become increasingly concerned about foreign ownership of agricultural land. According to the most recent U.S. Department of Agriculture (USDA) report, foreign owners (primarily Canadian) hold an interest in nearly 45 million acres of U.S. agricultural land.

Investment into data centers continues to increase significantly as the country builds out infrastructure to accommodate the digital economy and growth of artificial intelligence. Many states, including Texas, have now implemented various tax incentives to encourage investment in the state while simultaneously grappling with the taxable aspects of data center fuel. In November 2025, the

Solar developers contend with a wide array of challenges, from competing for viable project sites to combatting disinformation surrounding the expansion of clean energy development. With demand for energy rapidly growing across the nation, considering a full suite of project designs allows developers to put their best foot forward when collaborating with local stakeholders.

Although the use of a shared facilities agreement (SFA) for co-located energy projects is not a new concept, their use has increased significantly in recent years due to the rise in co-located generation, storage, and load infrastructure, particularly in the case of data centers. In general, an SFA grants each party a co-tenancy ownership interest in certain shared facilities, subject to detailed management, operations, and cost-sharing provisions, among other considerations.

Given the increasing frequency of their use, owners, operators, financing parties, and developers should understand when, why, and how SFAs can (or should) be used to avoid potential regulatory, operational, or cost-allocation issues with co-located projects.

Companies’ obligations to identify and disclose climate-related financial risks and climate data have become increasingly complex in recent years, both at the state and federal levels. The fate of federal climate disclosure rules remains unclear, with the Securities and Exchange Commission (SEC), other federal agencies, and the courts deferring action. Meanwhile, some states, such as California, are stepping in with their own robust requirements.

On December 18, 2025, the Federal Energy Regulatory Commission (FERC) directed PJM Interconnection, L.L.C. (PJM) to create new rules around the co-location of generation and data centers (FERC’s Dec. 18, 2025 Order, Docket Nos. EL25-49, AD24-11, EL25-20). With several proceedings pending at the Commission to address the growing demand for energy from large load entities—including major rulemaking proceeding directed by the Department of Energy (DOE) on October 23, 2025—FERC’s December 18 order offers the first window into how the Commission will address the challenges facing the nation’s electricity grid. These challenges include balancing resource adequacy, grid reliability, and fair cost allocation for any needed grid expansions to accommodate new AI-driven data centers. FERC is expected to issue a proposed rulemaking in the coming weeks with additional guidance on how it plans to shape the future of data center development in the U.S.

With any industry that has grown as quickly as renewable energy, safety is sometimes overlooked. The Occupational Safety and Health Administration (“OSHA”) classifies those working in the renewable energy industry as having a “green job.” The hazards of green jobs vary across the renewable energy field, whether in wind, solar, geo-thermal, or biofuel power generation companies. Ultimately, renewable energy companies must address both common workplace hazards and the emerging challenges unique to this developing industry.